The first part of #PaisaPolitics, an exclusive HuffPost India investigation into how the Modi government brought untraceable funds into Indian politics.

NEW DELHI — Days before unveiling electoral bonds, a secretive way to channel money to political parties, the Narendra Modi government pretended to ask the Reserve Bank of India (RBI) for its opinion, only to summarily dismiss the central bank’s reservations, previously unpublished documents obtained by HuffPost India reveal.

The undue haste shown by the government was striking given how serious the RBI’s objections were, the following account — based on these documents— shows.

Thus far, electoral bonds worth at least Rs 6,000 crore have been sold since March 2018. Of the first tranche, worth Rs 222 crore, the BJP has garnered 95% of the money according to data compiled by the Association for Democratic Reforms.

On a Saturday four days before Budget Day in 2017, a senior tax official spotted a wrinkle in the presentation the finance minister was scheduled to make before Parliament.

In his speech on February 1, 2017, Arun Jaitley, India’s finance minister at the time, planned to unveil “electoral bonds”: a controversial, legally-sanctioned instrument that would allow corporations and other legal entities to anonymously funnel unlimited amounts of money to political parties.

If written into law, these anonymised electoral bonds would legalise the influence of big business and open the opportunity for offshore money to pour into Indian politics.

But there was a hitch — the RBI had to be brought on board first.

For the latest news and more, follow HuffPost India on Twitter, Facebook, and subscribe to our newsletter.

Legalising these anonymous donations would need amendments to the Reserve Bank of India Act, the tax official wrote in a note dated January 28, 2017, to his superiors in the finance ministry. He drafted the proposed amendment and sent it up the ranks for the finance minister’s approval.

On the same day, at 1:45 pm, an official in the finance ministry shot off a perfunctory 5-line email, “requesting early comments” on the proposed amendment, to Rama Subramaniam Gandhi, then a deputy governor of RBI and second-in-command to Urjit Patel, the bank’s governor at the time.

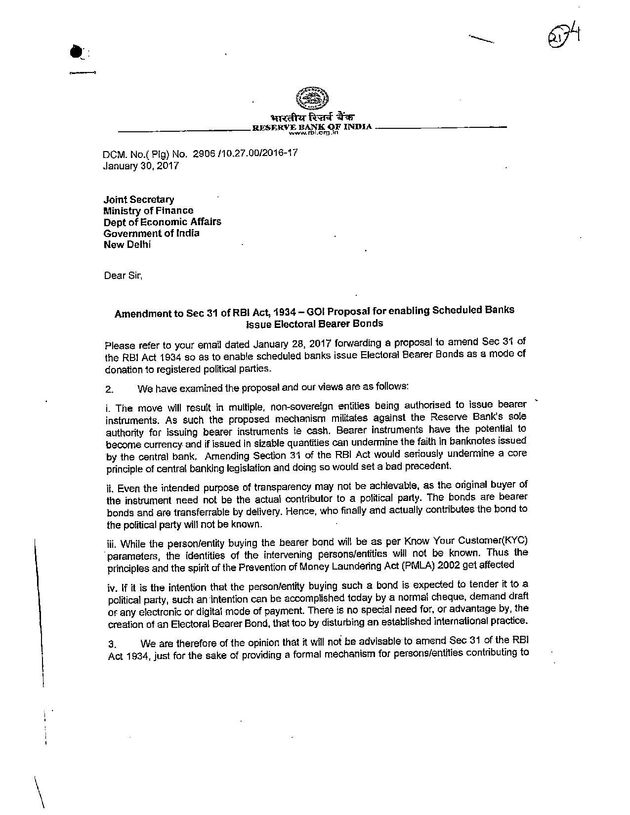

The RBI’s reply, recording its unequivocal opposition, was in by Monday, January 30, 2017. The RBI said that electoral bonds and the amendment to the RBI Act would set a “bad precedent” by encouraging money laundering and undermining faith in Indian banknotes, and would erode a core principle of central banking legislation.

Electoral bonds, the RBI said, would effectively be a type of “bearer bond” — a notoriously opaque financial instrument that carries no trace of its ownership.

“Bearer instruments have the potential to become currency and if issued in sizeable quantities can undermine faith in banknotes issued by RBI,” the bank wrote. “The bonds are bearer bonds and are transferable by delivery. Hence who finally and actually contributes the bond to the political party will not be known.”

Ordinarily, such strong opposition by the RBI would have made any administration pause. Usually, any government amends laws only after formal consultations with ministries and other government entities which may be impacted by the proposed changes or have a view on the matter.

But in the case of electoral bonds, the top echelons of the Modi government had already made up their mind.

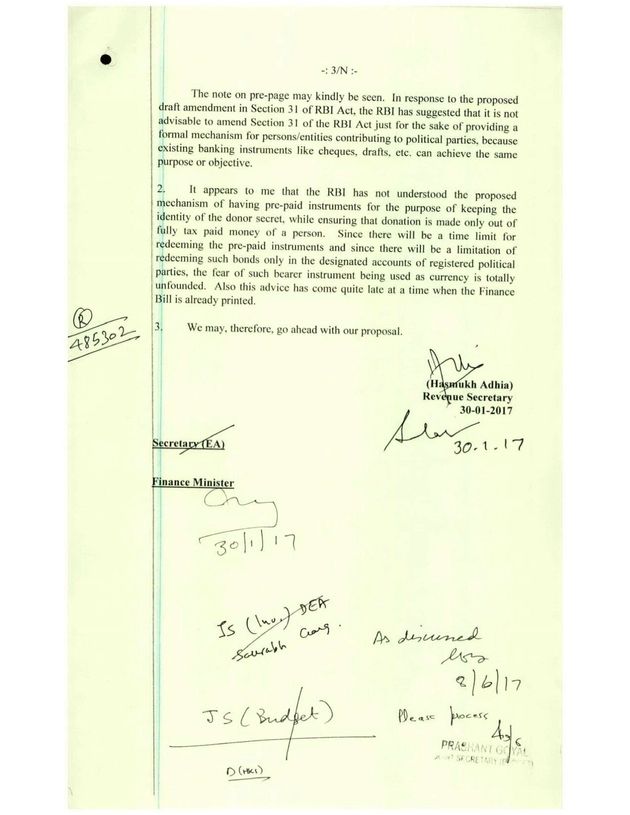

RBI’s concerns were summarily and swiftly dismissed by Hasmukh Adhia, who was then revenue secretary, in a single short paragraph on the same day the finance ministry received the central bank’s letter.

“It appears to me that the RBI has not understood the proposed mechanism of having pre-paid instruments for the purpose of keeping the identity of the donor secret, while ensuring the donation is made only out of fully tax paid money of a person,” began Adhia’s note to the secretary for economic affairs, Tapan Ray, and finance minister Jaitley.

Yet, rather than provide substantive arguments to counter the RBI’s concerns, his note revealed that the government had never been serious about RBI’s feedback to begin with.

“This advice has come quite late at a time when the Finance Bill is already printed.” Adhia wrote, despite the RBI responding on the first working day after it was asked for comment. “We may, therefore, go ahead with our proposal.”

On the same day, his colleague Tapan Ray agreed with Adhia. The file moved with lightning speed, and finance minister Jaitley signed off on it immediately.

Two days later, on February 1, 2017, Jaitley proposed the creation of electoral bonds, and the amendment to the RBI Act, as a means to introduce transparency and “cleanse the system of political funding in India”. The next month, the proposals passed into law with the passage of the Finance Bill 2017.

This seemingly innocuous tweak to the RBI Act and other amendments, rammed through in haste and with little consultation, was a windfall for India’s political parties—particularly the ruling Bharatiya Janata Party (BJP). Previously, Indian corporations had to give details of their political contributions in their annual statements of accounts. Also, they could not donate more than 7.5% of their annual profits averaged over three years. Foreign companies could not donate to Indian political parties at all.

The BJP-led government’s amendments changed all that. Indian companies, including shell companies which have no business but to channel money to political parties, individuals as well as other legal entities, such as trusts, can now anonymously buy unlimited amounts of electoral bonds and quietly hand them over to a political party of their choice to encash. Foreign companies can also now route money to Indian political parties.

This advice has come quite late at a time when the Finance Bill is already printed. We may, therefore, go ahead with our proposal.Hasmukh Adhia, former revenue secretary, on RBI's letter dated January 30, 2017

Now, as the Supreme Court considers the validity of the scheme, a tranche of documents obtained by transparency activist Commodore Lokesh Batra (Retd) reveal how the RBI — the guardian of India’s banking and financial system — was misled, ignored and overruled in the Modi government’s hurried quest to find legally-approved routes for not just Indian but also foreign companies to funnel money to political parties through an untraceable path.

Not only did the government dismiss the RBI’s initial objections to electoral bonds, it also ignored most of the bank’s subsequent suggestions to make the scheme less vulnerable to fraud and less prone to destabilising the Indian currency.

The finance ministry told HuffPost India via email that it would not be able to provide detailed responses to specific questions because it was busy preparing next year’s Union Budget, but said that all the decisions were taken “in good faith”.

″All the issues raised in the email are on the policy decisions taken by the then respective competent authorities. In this context, it may be mentioned that in the Government organisations all the decisions are taken in good faith and in the larger public interest. Interpretation of decisions taken may have different perspectives, hence an appropriate explanation may only be given, after taking into consideration all he aspects factored into the decisions making process,” said the finance ministry.

Bypassing the RBI

It was only after the government had got the concept of Electoral Bonds and opaque donations to political parties legalised by using its brute majority in Lok Sabha and questionably bypassing the Rajya Sabha, that it began to internally discuss how the bonds would really work.

Finance ministry mandarins began to fill in the details. At this stage, the government prepared a more detailed rebuttal to the RBI’s concerns on its internal records.

Where the RBI had questioned whether, contrary to the government’s claims, the bonds would actually bring transparency to political funding, the finance ministry officials said, “The secrecy of the donor is the core objective of the scheme of electoral bonds.”

To counter RBI’s warning that the bonds would seriously undermine a core principle of central banking and set a bad precedent, the finance ministry did not even try to provide an economic argument.

It bluntly noted, “Parliament is supreme and has the right to legislate on all subjects of governance including the RBI Act.”

By June 2017, four months after Jaitley’s electoral bonds announcement in Parliament, Economic Affairs Secretary Tapan Ray and his office had written up how the bonds would work in practice.

“The information regarding purchaser and payee shall be kept secret by the issuer bank,” the note that Ray agreed to said. “These details would also be beyond the purview of RTI.”

Political parties would be exempt from keeping records of names and addresses of those who contributed through electoral bonds, the note added.

This was in stark contrast to Jaitley’s section of the speech in Parliament on electoral bonds, which had begun with the title, “Transparency in Electoral Funding” and ended by claiming, “This reform will bring about greater transparency and accountability in political funding, while preventing future generation of black money”.

The note, contradicting the government’s claims in public of complete anonymity for donors, noted, “However, the records of the purchaser are always available in the banking channel and may be retrieved as and when required by enforcement agencies.”

This meant that only the government would know exactly who had bought these bonds.

Once the finance ministry had decided how the electoral bonds would function, a meeting was scheduled on Jaitley’s direction on July 19 2017, between finance ministry officials, the Election Commission of India and RBI to “finalise the structure of Electoral Bonds.” The Election Commission officials attended the meeting; the RBI did not.

On July 28 2017, RBI deputy governor B.P. Kanungo separately met the then economic affairs secretary S.C. Garg, who had taken over the role from Tapan Ray by then. On the same day, RBI governor Urjit Patel also met finance minister Jaitley to discuss the structure of electoral bonds, show records of the finance ministry.

In August, as a follow-up to the meetings between Jaitley and Urjit Patel, the RBI wrote to the finance ministry and pointed out the drawbacks of the scheme yet again.

There was an “inherent scope of misuse of such bonds for undesirable activities,” wrote Kanungo, the RBI Deputy Governor. “You may appreciate that globally there are hardly any precedents in recent times for issuance of bearer bonds.”

Yet, in a sign that the RBI knew it was fighting a losing battle, the bank made a last-ditch attempt to make the scheme a little less vulnerable to fraud and money-laundering.

“India can consider issuing the instruments, on a transitional basis,” the note concluded, and offered suggestions to limit the scope of misuse of the bonds: The bonds should only be valid for 15 days after they were issued, only those holding accounts with banks that are fully verified under the Know Your Customer norms should be allowed to buy these bonds; the bonds should be issued only twice a year for a short duration and only by the RBI Mumbai office.

Finally, the RBI also wanted a cap on the maximum aggregate value of bonds issued in a year.

“RBI has now appreciated the merits of the Electoral Bearer Bonds and is broadly in alignment with DEA’s proposal,” Economic Affairs Secretary Garg wrote in a note to the Finance Minister.“We could accept RBI’s suggestion on restricting the tenor of the Electoral Bearer Bonds to 15 days.”

Most other suggestions made by the central bank were ignored. The bond scheme was floated, allowing any Indian citizen, corporates, or other entities such as trusts and NGOs, to buy the bonds from SBI branches and donate them to political parties secretly.

An anonymous note

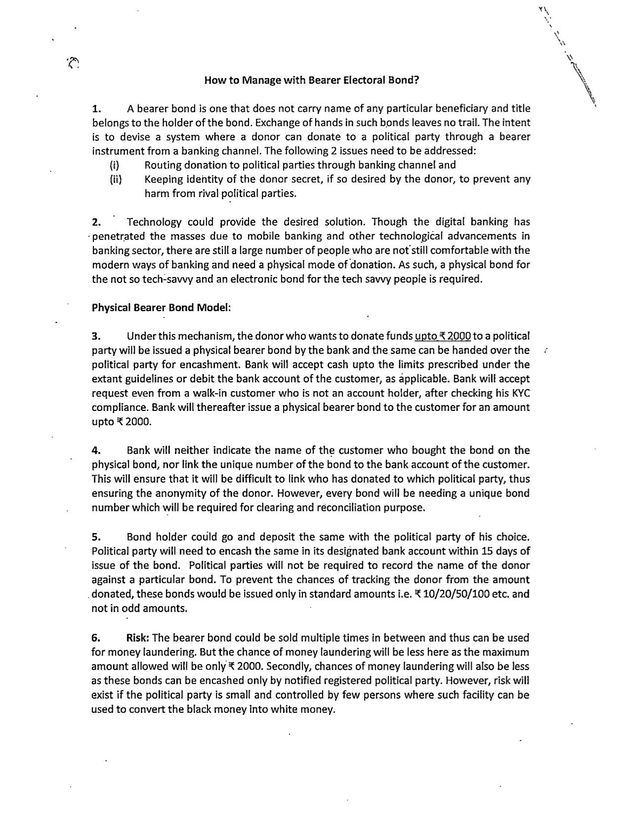

If the government had little interest in the RBI’s opposition to the electoral bond scheme, it also appeared to be taking advice from unusual quarters. Among the documents HuffPost India obtained under the RTI Act is what appears to be an early concept note on electoral bonds.

This early note is unlike most memos prepared by the Indian bureaucracy: it is undated, unsigned, and printed on a plain sheet of paper bearing no letterhead.

HuffPost India shared the note with one serving and one retired IAS official. One of them currently serves as secretary to the Union government and another has served in this position before. Both said on condition of anonymity that the note did not show the typical language that officers are expected to use.

“How to manage with Electoral Bond?” the note began, “A bearer bond is one that does not carry name of any particular beneficiary and title belongs to the holder of the bond. Exchange of hands in such bonds leaves no trail.”

The note suggested two kinds of electoral bonds that could run in parallel.

It recommended a “physical bearer bond model” for bonds up to Rs 2,000, though it also admitted there was a risk of this being used for money laundering. For amounts greater than Rs 2,000, the concept note suggested digitally generated bonds, managed by National Payments Corporation of India. The note admitted there was a chance for money laundering in this case as well.

“This reads more like it was written outside the government and given to the government as a concept note,” said the retired bureaucrat who reviewed the note. HuffPost India has been unable to independently verify the origins or author of this note.

Eventually the government did discard this mysterious note and formulate the current version of the electoral bond scheme.