Press Release

Date: 16th Oct, 2017

Analysis of Assets & Liabilities of National Parties – FY 2004-05 to 2015-16

Introduction

There are a set of accounting standards set for commercial, industrial and business enterprises and these accounting standards are issued by the Institute of Chartered Accountant of India (ICAI). Political parties fall under the non-commercial, non-industrial or non- business entity. Thus, the standard accounting formats of the other entities are not applicable to political parties.

The Election Commission of India (ECI) requested for recommendations from the ICAI to bring uniformity in the accounting and auditing practices of political parties. Thus, the “Guidance note on Accounting & Auditing of political parties” or the “Accounting guidelines” were formulated in February, 2012 by the ICAI on the request of the ECI, in order to improve accounting and auditing standards of political parties and improve transparency in their finances. These guidelines laid down principles of recognition, measurement and disclosure items of income, expenditure, assets and liabilities in the financial statements of political parties.

This report analyses the assets and liabilities declared by the seven National Parties (BJP, INC, NCP, BSP, CPI, CPM and AITC) between FY 2004-05 and 2015-16.

Executive Summary

Frequently asked questions

- What is a balance sheet?

Balance sheet contains information on three main financial aspects of the entity, which is a political party in this case. a) The “Assets” of the party are resources such as cash, their bank investments, moveable and immovable properties, vehicles, etc.; b) The “Capital” or “Reserve Fund” portion of the balance sheet is the accumulated wealth of the political party which is essentially assets minus any liabilities of the party; c) The “Liabilities” of a political party includes borrowings from banks, unsecured loans, access to overdraft facilities, etc.

- What is special about assets and liabilities/ income & expenditure of political parties?

The accounting standards were created keeping in mind the nature of activities of the entities, be it commercial, industrial or business. While political parties do not perform any commercial activities, the purpose of the accounting standard i.e. maintain uniformity in presentation, is kept intact by merely modifying the terminology such as “Income and Expenditure” in place of “Profit and Loss”.

- What are ECI’s transparency guidelines?

Article 324 of the Constitution empowers the ECI with plenary powers which was established in the Supreme Court judgement (AIR 1978 SC 851) by stating that the Commission has the powers to fill any legal vacuum so as to promote free and fair elections. The transparency guidelines, circulated in 2014, were lawful instructions issued after consultation with all recognised parties and hence are binding. These guidelines were formulated to improve financial transparency in political parties and strongly advised the parties to follow the ICAI guidelines formulated and circulated in February, 2012.

- What information is captured in this report?

The assets, liabilities and capital declared by the seven National Parties (BJP, INC, NCP, BSP, CPI, CPM and AITC) between FY 2004-05 and 2015-16 have been taken up for analysis in this report. The assets include fixed assets, loans & advances, deposits made, investments, etc. while the liabilities include bank borrowings, sundry creditors, overdrafts, other liabilities, etc. The capital/ reserve fund is the amount set aside by the parties after subtracting liabilities from the total assets, every year, for party expenditure.

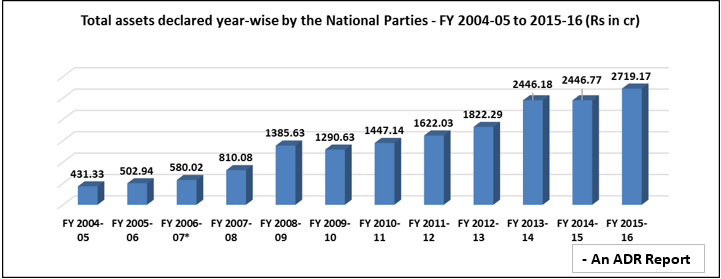

Declaration of assets by the National Parties – FY 2004-05 to 2015-16

- The average total assets declared by the seven National Parties during FY 2004-05 was Rs 61.62 cr which increased to Rs 388.45 cr during FY 2015-16.

- A decrease of Rs 95 cr was declared by the parties together between FY 2008-09 and 2009-10 while an increase of Rs 156.51 cr was declared between FY 2009-10 and 2010-11.

*The balance sheet of BSP for the FY 2006-07 is unavailable in the public domain

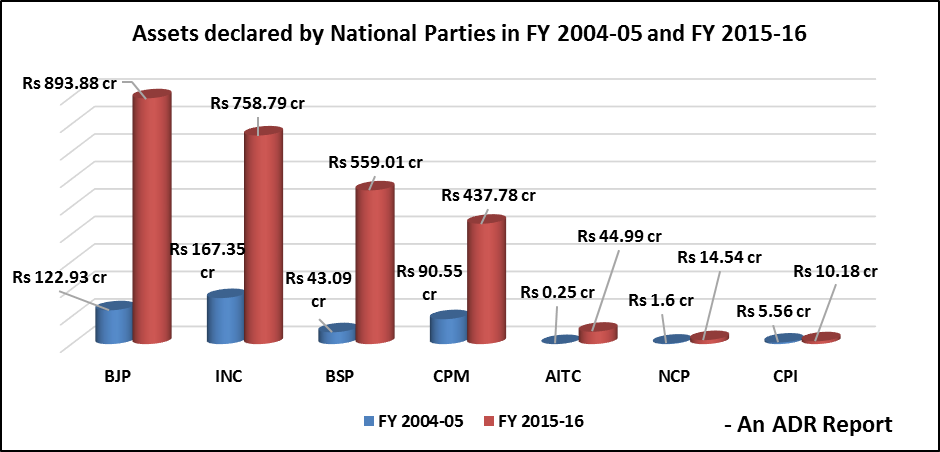

- During FY 2004-05, the declared asset of BJP was Rs 122.93 cr which increased by 15% to Rs 893.88 cr during FY 2015-16.

- CPM and AITC are the only two National Parties to show a steady increase in their annual declared assets. The total assets of CPM between FY 2004-05 & 2015-16 increased by 383.47% (Rs 90.55 cr to Rs 437.78 cr) while that of AITC increased from Rs 0.25 cr to Rs 44.99 cr (by 17896%).

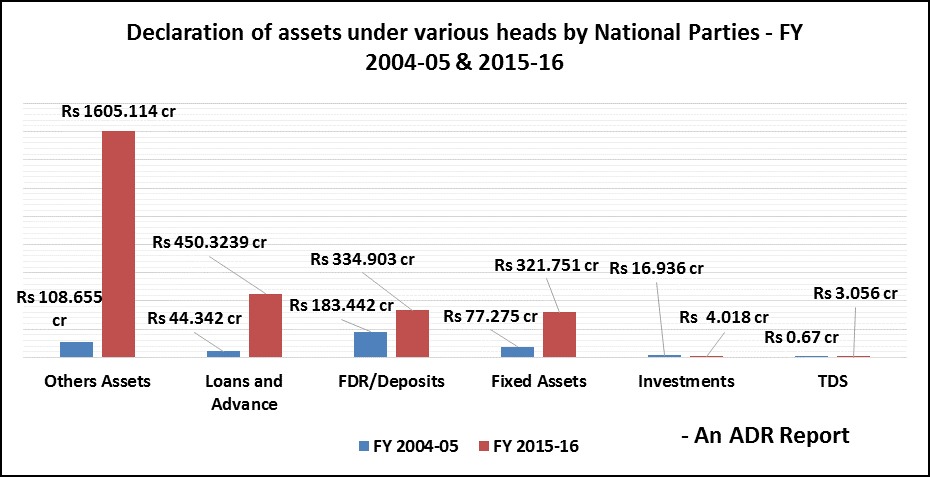

- The assets declared by National Parties fall under 6 major heads: fixed assets, loans & advances, FDR/ deposits, TDS, Investments and other assets.

- During FY 2004-05, the National Parties declared maximum assets under FDR/ deposits which amounted to Rs 183.442 cr. This constituted 42.53% of total assets declared by the parties under various heads.

- During FY 2015-16, the highest asset category is other assets under which the parties have declared holding Rs 1605.114 cr which formed 59% of the total assets declared under various heads by the parties.

- It is to be noted that the only asset category to show a reduction in value was “Investments”. During FY 2004-05, parties invested a total of Rs 16.936 cr whose current value stands at Rs 4.018 cr.

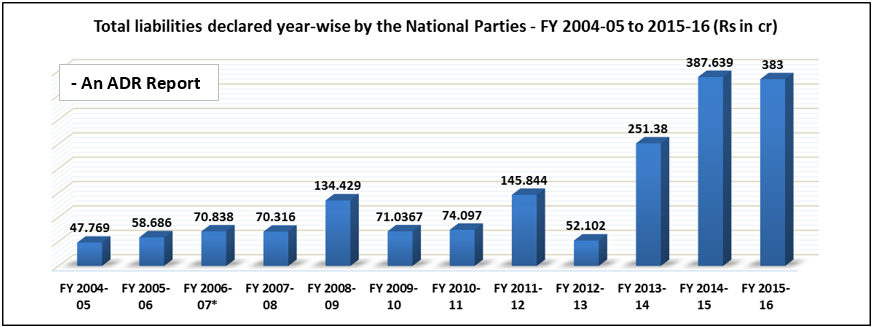

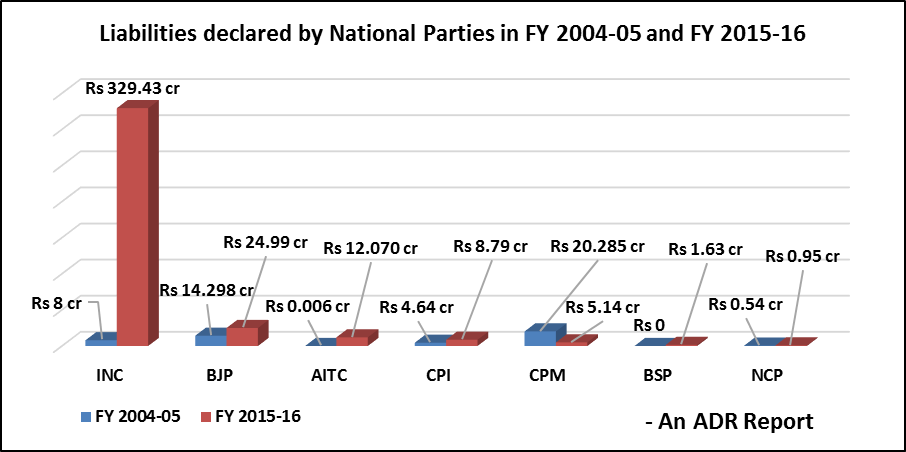

Declaration of liabilities by National Parties – FY 2004-05 to 2015-16

- The seven National Parties declared a total of Rs 47.77 cr as liabilities during FY 2004-05, an average of Rs 6.82 cr per party. CPM declared highest liabilities of Rs 20.285 cr followed by BJP with Rs 14.298 cr.

- A marked increase in total liabilities of parties is observed during FY 2008-09 (Rs 134.429 cr), 2011-12 (Rs 145.844 cr) & 2014-15 (Rs 387.639 cr).

*The balance sheet of BSP for the FY 2006-07 is unavailable in the public domain

- The total liabilities for FY 2015-16 declared by the National Parties is Rs 383 cr, an average of Rs 54.71 cr per party. INC declared the highest liabilities of Rs 329.43 cr followed by BJP with Rs 24.99 cr.

- CPM is the only party to declare a decrease in liabilities from Rs 20.285 cr during FY 2004-05 to Rs 5.14 cr during FY 2015-16.

- The liabilities declared by National Parties fall under 2 major heads: borrowings (from banks, overdraft facilities and sundry creditors) and other liabilities.

- During FY 2004-05, the National Parties declared maximum liabilities under “other liabilities” - Rs 31.43 cr while during FY 2015-16, the highest liabilities were “borrowings” where the parties declared a total of Rs 333.14 cr.

- CPM has declared nil liabilities under “borrowings” for all years except during FY 2010-11 when the party declared Rs 44.70 lakhs under this head. “Other liabilities” amount to Rs 5.14 cr for the party for FY 2015-16.

- Highest liabilities declared by INC was during FY 2014-15 during which the party had liabilities amounting to Rs 327.54 cr under “borrowings”.

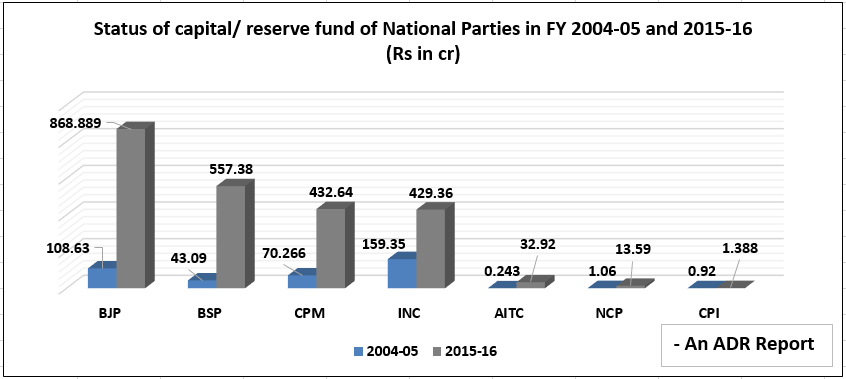

Capital declared by National Parties – FY 2004-05 to 2015-16

- The total Capital/ Reserve fund set aside by the National Parties during FY 2004-05 was Rs 383.56 cr, and Rs 2336.17 cr for FY 2015-16.

- BJP has the highest capital at present after declaring Rs 868.889 cr followed by Rs 557.38 cr of BSP and Rs 432.64 cr of

- The reserve funds of BJP, between FY 2004-05 and 2015-16 increased by 700% while that of INC increased by 169%. Highest percentage increase was seen in AITC with 13447% followed by BSP with 1194%.

Observations & Recommendations of ADR

Observations

- According to the ICAI guidelines, parties are directed to declare details of the financial institutions, banks or agencies from whom loans were taken. The guidelines specify that the parties should state the “terms of repayment of term loans” on the basis of due date such as a year, 1-5 years or payable after 5 years – not declared by the National Parties.

- Details of fixed assets received as donation by the parties should be declared such as original cost of the asset, any additions or deductions, depreciation written off, cost of construction, etc. The same should also be declared for fixed assets purchased by the political parties - not all National Parties declared this information.

- Details of loans given by the parties in cash/ kind should be specified and if it constitutes more than 10% of the total loans, nature and amount of such loans should be declared specifically by the parties - not declared by the National Parties.

- ICAI guidelines on auditing of political parties which were also endorsed by the ECI in order to improve transparency in the finances of political parties, remain guidelines only and have not been actively taken up by the political parties as a mandatory procedure to disclose details of their income. These guidelines were meant to standardize the format of financial statements of parties apart from improving disclosureof income, expenditure, assets and liabilities of the unique association, political parties. Details of disclosure included:

- Classification and disclosure of details of donors (individuals, companies, institutions and others) – classification not declared by the National Parties.

- Revenue from issuance of coupons of different denominations to be disclosed separately – not declared by the National Parties.

Recommendations

- Changing of auditorsevery three years:

- The amended Companies Act, 2013, which came into force on 29th Aug, 2013, stated that no Company shall have an auditor for more than 5 years but this rule was not applied for political parties. Hence, designating a firm/person for auditing of accounts of parties for long durations is not desirable as there is a feasibility of making finances of parties as opaque as possible.

- Indian laws do not permit foreign auditing firms to operate directly in India but they might have a tie-up with domestic auditing firms which may enable foreign companies to have access to the parties’ internal accounting.

- The 255th Law Commission report has recommended that the accounts of political parties be “audited by a qualified and practicing Chartered Accountant from a panel of such accountants maintained for the purpose by the Comptroller and Auditor General.” However as per the current practice, political parties choose their auditors entirely on their own. This needs to change.

- As the income-expenditure statements of political parties are assessed rarely (even those of National Parties), authenticity of the accounts submitted remains doubtful. When the authenticity is not verified, the auditors who might be under-reporting the accounts, remain out of purview of punishment. With online submission of IT Returns, political parties do not submit details of income, expenditure and assets and liabilities as attachments. Thus, the IT department too does not have enough information on the finances of political parties! Annual scrutiny of documents submitted by political parties is recommended.

- The 170th Law Commission report recommended introduction of Section 78A in the RPA and proposed penalties for political parties defaulting in the maintenance of accounts. This needs to be introduced and implemented.

- Section 276CC of the IT Act penalizes individuals who fail to submit their IT returns. Similar legal provisions should be applicable to political parties too. Supreme Court judgement in Common Cause vs. Union of India & ors. had stated that when parties default in filing their returns, prima facie they violate provision of IT Act.

Contact Details

Media and Journalist Helpline: +91 80103 94248, Email: [email protected]

|

Ms Ujjaini Halim Coordinator – West Bengal Election Watch 033-24836491 98302 99326 |

Maj. Gen Anil Verma (Retd.) Head - NEW/ADR +91 11 4165 4200 +91 88264 79910 |

Prof Jagdeep Chhokar IIM Ahmedabad (Retd.) Founder Member- NEW/ADR +91 99996 20944 |

Prof Trilochan Sastry IIM Bangalore Founder Member- NEW/ADR +91 94483 53285 |